Paris Protesters Invade Blackrock HQ

Pension Reform backlash escalates as protesters briefly invade Blackrock headquarters.

Dear Investors,

In a scene that could have been from Netflix’s “Money Heist,” Dozens of French trade union protesters invaded the central Paris building that houses the office of U.S.-based investment firm BlackRock on April 6th, chanting slogans and setting off firecrackers. Videos posted on social media show protesters holding red flares and firing smoke bombs as they entered the Centorial office block near the Opéra Garnier opera house. Around 100 people, including representatives of several labor unions, were on the ground floor of the building for about 10 minutes, chanting anti-reform slogans.

Although BlackRock has played no part in the pension reforms, workers targeted the company because of its work for private pension funds. The government wants to discard pensions and force people to fund their retirement with private pension funds, which protestors say would only benefit the rich.

The French government's proposed pension reform, which seeks to increase the minimum retirement age from 62 to 64, has stirred up a lot of public outrage and resulted in massive protests across the country. Millions of people have been demonstrating on the streets in recent months, leading to the closure of schools, public transit, and major cultural attractions like the Eiffel Tower and the Louvre. As a result of the protests, heaps of garbage have piled up on the streets, with some being set on fire by demonstrators.

Understanding the Proposed Pension Reform

The French government estimates that the proposed pension reforms will result in €17.7 billion in annual pension contributions by 2030, with the goal of ensuring that the pensions of the poorest 30% of retirees are better protected. Unlike many other European countries, France has a system in which the contributions of current workers directly fund the pensions of current retirees, without relying on private pension funds. The government claims that this change is essential to prevent a funding deficit, but the reforms have generated strong opposition from workers, particularly as inflation has been rising, making it more difficult for people to make ends meet. The government triggered special constitutional powers last month to push through the legislation without a vote, which has further fuelled the protests.

The centerpiece of the reforms is a rise in the minimum pension age from 62 to 64, and an accelerated increase in the required number of annual contributions from 41 years to 43 to qualify for a full pension. This is still lower than most of Europe, where the retirement age is 65 and is being raised to 67 in some countries. Macron has been determined not to be pushed around by the protesters, as he believes that pension reform is essential to address the country's financing gap, given that France spends nearly 14% of its GDP on public pensions.

The proposed reforms have also sparked debate about the use of constitutional provisions to impose decisions against the will of the people. While Macron's top-down governing style has irked many, the use of these provisions to push through the legislation has reinforced the perception that he is not listening to the opposition. Despite the opposition, raising the retirement age appears to be the soundest way to close the financing gap, as seen in other European countries.

Why Is This Happening?

Many believe that the root cause of the issue at hand extends beyond the matter of pensions alone. Rather, it stems from the widening wealth disparity, the devaluation of savings due to inflation, and a general loss of trust in centralised government.

Can we blame the general populace for their frustration? After all, there's a segment of society that continues to grow wealthier, upgrading their cars, clothes, shoes, and homes while devising increasingly complex tax evasion strategies. In contrast, ordinary workers, who dutifully pay taxes and work well into their 60s, now face delayed retirement and watch helplessly as their hard-earned savings are eroded by inflation.

Unfortunately, I think France is just one of many examples of people fighting back against a system that doesn’t serve them over he coming years.

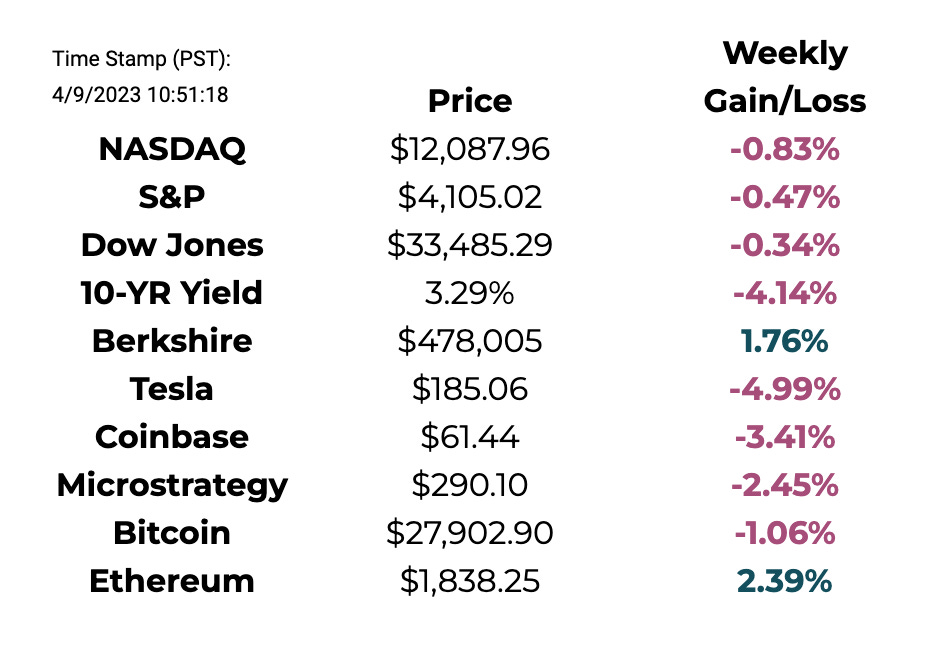

This Week By the Numbers 📈

The market further tightened following the Federal Reserve's comments that interest rates will exceed 5% and remain at that level for an extended period to counter inflation.

Top Stories 🗞️

Head of Thailand’s Opposition Party Promises $300 Crypto Airdrop if Elected Prime Minister

A contender to be the prime minister of Thailand is promising every citizen 10,000 Thai Baht (approximately $300) in digital currency if his party forms a government following a general election scheduled for May. The Bangkok Post reports that real estate mogul turned candidate Srettha Thavisin promises a basic-income style economic stimulus package via “digital currency” should his party, Pheu Thai, win the next election. Thavisin says the measure will provide some economic relief to Thais that are trapped with some of the highest household debt in the region.

DeSantis and RFK Jr. warn against Fed’s digital plans in warning of government overreach

Florida Gov. Ron DeSantis alleged last weekend that a Fed-made digital U.S. dollar would let the government block transactions like buying a rifle or filling up with “too much gas.” He added, speaking at a Pennsylvania conference on Saturday, “They are going to try to impose an ESG agenda,” referring to private sector policies aimed at advancing environmental, social and governance principles, which conservative lawmakers across the country have been pushing to curb. “It is ceding the power of our financial freedom to a central bank which does not have our interests at heart,” DeSantis said. The Fed is readying its “FedNow” initiative, which aims to shorten the time it takes for banks to send funds to other banks, for a planned July rollout. Separately, it has also been exploring the possibility of issuing a digital version of the dollar that households could readily use instead of cash.

Three Congressmen Introduce Gold Standard Bill to Stabilize the Dollar's Value

As America faces the twin threats of inflation and bank failures, three U.S. congressmen introduced a pivotal sound money bill that would enable the Federal Reserve note "dollar" to regain stable footing for the first time in more than half a century. Rep. Alex Mooney (R-WV) - joined by Reps. Andy Biggs (R-AZ) and Paul Gosar (R-AZ) - introduced H.R. 2435, the "Gold Standard Restoration Act." Upon passage of H.R. 2435, the U.S. Treasury and the Federal Reserve are given 24 months to publicly disclose all gold holdings and gold transactions, after which time the Federal Reserve note "dollar" would be formally repegged to a fixed weight of gold at its then-market price. Federal Reserve notes would become fully redeemable for and exchangeable with gold at the new price, with the U.S. Treasury and its gold reserves backstopping Federal Reserve Banks as guarantor. Monetary experts have noted a return to a gold standard would substantially curtail the economic damage caused by inflation, runaway federal debt, and monetary system instability.

Russia shifts to Dubai benchmark in Indian oil deal

Russia's largest oil producer Rosneft (ROSN.MM) and India's top refiner Indian Oil Corp (IOC.NS) agreed to use the Asia-focused Dubai oil price benchmark in their latest deal to deliver Russian oil to India. The decision by the two state-controlled companies to abandon the Europe-dominated Brent benchmark is part of a shift of Russia's oil sales towards Asia after Europe shunned Russian oil following Russia's invasion of Ukraine more than a year ago. Both benchmarks are denominated in dollars and set by S&P Platts, a unit of U.S.-based S&P Global Inc (SPGI.N), but Brent is mostly used by European oil majors and traders, whereas Dubai is heavily influenced by Asian and Middle Eastern oil trading. Rosneft's chief executive Igor Sechin said in February that the price of Russian oil would be determined outside of Europe as Asia has emerged as largest buyer of Russian oil since the West imposed progressively tighter sanctions on the export.

Study claims 99.5% of crypto investors did not pay taxes in 2022

Swedish crypto tax firm Divly has released a new report that estimates that only 0.53% of crypto investors globally paid tax on their crypto in 2022 — however, tax experts have cast doubt on the figures and methodology. The report estimates that Finland has the highest proportion of crypto investors who paid the required taxes on crypto in 2022 at 4.09%, with Australia following closely behind with 3.65%. The United States ranked 10th on the list, with an estimated 1.62% of crypto holders paying taxes, while India, Indonesia and the Philippines had the lowest rates of tax-paying crypto investors, at just 0.07%, 0.04% and 0.03%, respectively.

Thank you for reading this week’s edition of the Myth of Money.🚀

Until next week,

Tatiana Koffman

About the Author: Tatiana Koffman

Hi there and thanks for reading! If you stumble upon my newsletter, you will notice that I write about money, economics, and technology. I hold a JD/MBA and spent my career in Capital Markets working across Mergers & Acquisitions, Derivatives, Venture Capital, and Cryptocurrencies. I write to make financial topics more accessible and create equal opportunity for the next generation of investors. I have personally invested in 20+ companies and funds (👉 my portfolio).

It’s definitely about more than raising the pension age a couple years. I think there is a lot of resentment in the west about what our governments are forcing on us... interesting to see how this plays out.

I like your tone , style , interesting, straight to the point with a wide scope , but not too wide .

As a CEO entrepreneur.. with long days and weeks ;) , it is good to have a synthesis . Thank you